Colorado’s state and local tax burden was the sixth lowest in the U.S. in fiscal 2016, according to a recent report produced Key Policy Data (KPD), a joint venture between Public Choice Analytics and Visigov.

The report relies on an income-based analysis dividing the state’s total tax collections by its private sector personal income. The national average using this methodology was an overall local and state tax burden of 14.3 percent of income; Colorado’s was 11.8.

KPD compared the burden of tax systems across states by measuring tax collections against the size of the economy. It defines this as the “total private sector share of personal income, which is personal income minus government compensation and personal current transfer receipts” such as Social Security, Medicare and Medicaid.

Colorado lawmakers have all but signed off on the biggest budget in state history. The $28.9 billion spending plan invests taxpayer dollars in roads, schools and the state’s troubled pension fund.

Unlike in previous years, lawmakers had a $1.3 billion surplus to split between their different priorities. The extra money is thanks to a booming a economy and the federal tax reform package, according to state economists. While a surplus has eased tensions among lawmakers jockeying for priorities, it also has them scrambling for the extra dollars.

The Senate added a number of changes to the budget Wednesday night. The chamber is scheduled to take a final vote on it’s version this week before a bipartisan committee begins ironing differences with the House version. The deadline for final passage is the end of next week. Here’s where the money is — and isn’t — headed.

No TABOR Refund

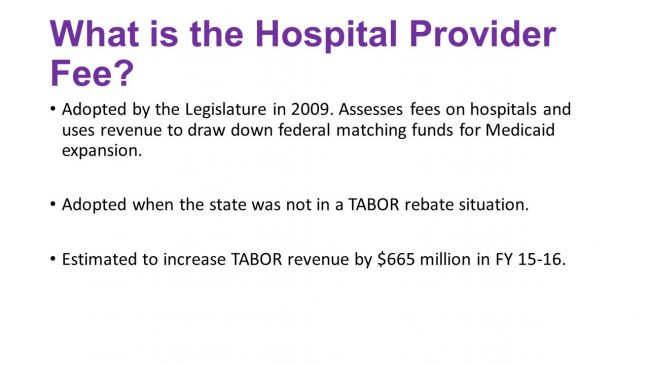

In Colorado, the Taxpayers’ Bill Of Rightslimits the amount of money lawmakers can spend before they have to supply refunds to taxpayers. Lawmakers don’t expect to hit the TABOR cap over the next fiscal year, so Coloradans won’t be getting a refund check next year. Part of the reason for that has to do with a major financial compromise struck last year. It recategorized a fee paid by hospitals, which created room for spending beneath the TABOR limit.

Fix Roads And Bridges

The budget allocates $495 billion for one-time spending on road projects. That’s a fraction of the $9 billion the Colorado Department of Transportation says it needs to modernize transportation infrastructure around the state. But the spending is in line with a request from the governor and a compromise transportation bill approved in the Senate last week. That plan would use the money to buy time for voters to consider a citizen initiative in November to raise sales taxes for road funding. If that fails, the compromise would trigger another initiative asking voters for new transportation bonds in 2019. Continue reading →

You know that your TABOR Foundation filed a lawsuit to stop the collection of the Hospital Provider tax and program until the new tax receives its required voter approval. We also had to amend the lawsuit to include all the wrong-headed, errant and unconstitutional provisions that affected the program with the passage of Senate Bill 267 last year. That measure will allow an increase of state taxes of (at least) $400 million per year, without the required TABOR vote. It also moved the welfare program that is the Hospital Provider fund off the books by renaming it as a government business.

We wanted to let you know that there has been significant activity on that lawsuit. It had been filed originally in 2015 but was not taken up by the Court for 18 months. Within the past several months, our attorneys at Mountain States Legal Foundation filed the amended complaint. They have answered copious number of briefs to:

obtain permission to make that filing,

to resist unsuccessfully the addition as Defendants of the Hospital Association, and

to add to our own list of Plaintiffs

In addition, a lot more activity has taken place with the procedure of Discovery. Just last week, I was deposed for nearly four hours by opposition attorneys, and another TABOR Foundation Director, Rebecca Sopkin, withstood another two hours of grilling. Our attorneys have taken depositions from the Defendants.

Our attorneys must also deal with the Defendants’ motion to dismiss the lawsuit altogether, as they allege among other things, that there is no remedy (“relief”) for the problems we have cited. There is also an important motion for summary judgment that is in process. Unless one of those two motions is successful, we will see this lawsuit go to trial in late June.

We’ll try to keep you apprised of further developments as they occur. The speed that new steps are occurring and the demands on our volunteer time are such that we have been running out of time to inform you in a timely manner.

Some Republican state legislators remind us that no one’s life is a complete waste — some simply serve as bad examples. One of those bad examples can be found in Colorado. (AP Photo/P. Solomon Banda)

Congress just proved an amazing thing happens when Republicans remember to govern as Reagan Republicans.

The most substantial tax overhaul since the Reagan years has sparked our economy. Republicans in Congress gathered the courage to face down the pro-tax media, special interests, and the opposition of every single Democrat in Congress to help families keep more of what they earn. Already tax reform has resulted in at least 285 companies announcing wage increases, bonuses, and higher 401(k) matches for 3 million workers. Utility companies are reducing rates in response to the Tax Cuts and Jobs Act. Continue reading →

To comprehend how that’s possible, we need to understand the largest betrayal of Republican values in Colorado political history: the tax-hiking, debt-raising, TABOR-busting Senate Bill 267, sponsored by Republican state Sen. Jerry Sonnenberg and enabled by the schizophrenic leadership of Senate President Kevin Grantham.

The beauty of our Taxpayer’s Bill of Rights is that taxes and debt can grow as high as any communist would like, all you have to do is ask the voters first. But elected officials, doing their best Bernie Madoff, don’t want to ask for consent when they know the answer is going to be “no.” They re-label taxes as “fees” and debt as “certificates of participation,” so the Colorado Supreme Court lets them take our money without our voter consent.

In 2009, without asking, the state forced an extra tax on us when we’re sick and have to go to the hospital. In their best George Orwell, the legislature named this tax “The Hospital Provider Fee,” as if hospitals, not patients, pay it. The new “fee” generated more than $650 million in 2016, pushing Colorado’s revenue over its TABOR cap.

Legislators find way to restore pot-tax funding to RTD, museums

A RTD train sits at the corporate office, located between the Evans and Broadway stations.

By Ed Sealover – Reporter, Denver Business Journal

Jan 30, 2018

Regional Transportation District trains, Scientific and Cultural Facilities District museums and other beneficiaries of special-district funding soon will be on a path to again receive the revenues from retail marijuana sales that they’d been losing since July.

Colorado senators on Tuesday approved a “fix” for the language that has left those districts unable to collect sales taxes for cannabis sales within their district since shortly after an omnibus funding bill from the 2017 session was signed into law. Affected organizations have warned that while the problem has not led to program cuts yet, it could do so in the future if it’s not remedied.

The fix to the error made in Senate Bill 267 is not one with unanimous support, having passed to the House Tuesday on a final vote of 24-10. Republican leaders warned not only that they feel the bill is unconstitutional, but that districts that re-start the collection of marijuana taxes without a vote of the people may be challenged in court.

Still, the organizations likely to begin receiving more money in the near future cheered Thursday’s vote to pass Senate Bill 88 out of the Republican-majority Senate and onto the Democrat-led House, where leaders have expressed support for the fix.

“Right now we’ve been able to absorb that loss of revenue. But long-term it’s definitely going to affect what we’re able to do,” said Scott Reed, assistant general manager for communications at RTD, which has lost about $500,000 a month. “This is a step in the right direction to correct the inadvertent mistake from Senate Bill 267.” Continue reading →

When El Paso County asked voters in 2012 to impose a .23 percent sales tax to fund the Sheriff’s Office, the ballot question said the new tax would raise “approximately $17 million” annually.

Turns out, it raised $17,898,721 in the first year and even more every year since. But the county hasn’t made a move to either lower the tax or refund the extra money.

Now, anti-taxer Douglas Bruce wants to force the issue. He filed a lawsuit on Dec. 26 seeking a refund to taxpayers of that roughly $900,000, with 10 percent interest per year for four years, and a reduction in the tax rate to prevent future excess collections.

That’s what he says is required by the Taxpayer’s Bill of Rights, a state constitutional amendment that Bruce authored, which was adopted by voters in 1992. TABOR states that if a tax increase generates revenue that exceeds an estimate contained in the election notice ballot measure, the tax rate must be lowered in subsequent years and the excess refunded in the next fiscal year.

“They are only supposed to get whatever they asked for,” Bruce says, noting in the lawsuit that TABOR provisions were designed to “prevent government from ‘lowballing’ the true cost of what it requests in order to lure voters to support it.” Continue reading →

Where do we stand today on the Hospital Provider charge lawsuit?

There has been a flurry of activity. The original lawsuit (“Complaint”) languished in the Court without resolution for more than 18 months. Then, late in the session the legislature passed the infamous SB267, which among other steps, increased future state taxes up to $400 million per year without voter approval, and moved the Hospital Provider Fund off the books and supposedly redefined that welfare program as a government business.

The TABOR Foundation’s attorneys at Mountain States filed an amended Complaint to address the additional unconstitutional provisions of SB267. More recently Mountain States met the deadlines imposed by the Court for any further amendments. The revised Complaint (attached here) broadens the parties with standing to include individuals who paid the Hospital Provider charge, Rebecca Sopkin and Scott Rankin, and added the Colorado Union of Taxpayers; a change that the Board approved earlier this year. There was some refinement of the arguments.

Some uncertainty exists about how the lawsuit will proceed. There is a Defendant’s Motion to Dismiss that will probably be addressed in January. However, the Court has allowed the lawsuit to proceed, so Steve Lechner will simultaneously be preparing the case for the June Hearing. Motions for discovery were issued timely and Defendants’ (now both the State and the Hospital Association) information will be gathered.

Stay tuned; this lawsuit is now moving along quickly.

At 6:00 PM tonight, Penn Pfiffner talks about TABOR First Amendment Rights Vs Campaign Disclosures … The Goldwater Institute Takes To The Courts To Protect Free Speech

If you want to have friends watch …. we do Facebook Live and Live Stream

Lauren Neidel Rejoins Us To Discuss The Controversies Surrounding The Emergence Of The Progressive Democratic Movement

Real Issues. Intelligent Conversation.

We Are Outrage Porn Free, Civilly Disobedient Media

Friday Night … Candidates! Invenergy, Invenergy, Invenergy … Religion & Politics … Sweet Home Alabama … & More! All Times Are Eastern

At 6:00 PM Penn Pfiffner TABOR First Amendment Rights Vs Campaign Disclosures … The Goldwater Institute Takes To The Courts To Protect Free Speech

At 6:30 PM: Bill Hunt – Newly Announced Candidate For Rhode Island General Assembly District 68. We’ll discuss his Libertarian Philosophy, Plus! His Take On State & East Bay Issues

At 7:30: Progressive Activist Lauren Niedel Talks Women’s Caucus

At 8PM: Hesham El-Meligy Co-Founder Muslims For Liberty. Topics Will Include An Analysis Of the Muslim Faith … And It’s Interrelationship With Civil Liberties & The American Liberty Movement. Plus! Jerusalem … American Intervention …

EVENING TALK RADIO LIVES ON!

The Coalition Talk Radio 2.0 Live! On The GoLocalLive Media Network Watch On: http://www.facebook.com/TheCoalitionRadio/

Friday’s From 6-9PM

Matt Miller, an attorney for the Phoenix-based Goldwater Institute,= discusses a lawsuit filed by the group challenging part of the Denver campaign finance law. With him outside the Denver City and County Building on Dec. 13, 2017, are Marty Neilson, left, of the Colorado Union of Taxpayers, and Penn R. Pfiffner from the TABOR Committee.

Two conservative taxpayer advocacy groups filed suit Wednesday against Denver over campaign finance disclosure rules that they say will violate the privacy rights of their donors when the groups get involved in city elections.

The lawsuit, filed by the Phoenix-based Goldwater Institute on behalf of the two groups, says changes approved by the City Council in September violate the free speech provision of the First Amendment. The city ordinance requires clubs, associations, corporations and groups that advocate for or against local ballot measures to meet the disclosure requirements of issue committees once they raise and spend at least $500.

Once it passes that threshold, an issue committee must identify by name and address each donor who gave $50 or more within that calendar year.

“We have donors who like to remain anonymous, and we’d like to honor their requests,” said Marty Neilson of the Colorado Union of Taxpayers. “We think this is an unconstitutional ordinance.”