Colorado Taxpayer’s Bill of Rights by the Independence Institute

Mar. 2, 2017,

The Colorado Court of Appeals on Thursday sent a case back to a lower court that could leave future funding for state and local elections in jeopardy.

The case, filed by the National Federation of Independent Business, claims that businesses carry an unfair burden of the cost of funding state and county elections. The business group hopes to reclaim the revenue, which would potentially throw elections into flux.

The appellate decision is not immediate cause for concern for state officials, as the court is only requiring the lower court to gather more information before making a decision.

“We reverse the summary judgment and remand to the district court with directions to hold further proceedings to determine whether the Business and Licensing charges have been adjusted or increased since the passage of TABOR in 1992, so as to require voter approval for the adjustments,” the Court of Appeals wrote in its decision.

“Depending on the court’s determination, it may need to reach the issue as to whether the Business and Licensing charges constitute a tax or a fee.”

That last statement by the court represents the heart of the case and what could cast uncertainty over elections in Colorado. More broadly, it could throw a curveball to all state departments that are funded by fees.

The question is whether business filings collected by the department qualify as a “fee” or a “tax.”

Taxpayers Bill of Rights foundation member Penn R. Pfiffner discusses TABOR at the event “Social Perspectives: conversation, debate and understanding.” The event was held by the Denver Post at the Denver Press Club on Feb. 28.

Photo by Taelyn Livingston • tliving4@msudenver.edu

Kristi Hargrove voted for Donald Trump in the last election. From Crested Butte, which she calls a liberal town, she identifies as a proud Republican.

“My daughter came home from school, she was in middle school, complaining about how cold she was at school,” Hargrove said. It was around 2003. “I said to her, well wear more clothes, because you never put on enough clothes.”

However, when Hargrove went to work on a student directory for her P.T.A., she had trouble because her fingers were freezing. After confronting the principle, she found out the school had turned down the utilities.

“We live in a fairly affluent area and I thought that was ridiculous,” she said. “My comment to her was, ‘who’s wasting money?’” Continue reading

State Rep. Dan Thurlow, R-Grand Junction, and state Sen. Larry Crowder, R-Alamosa, have introduced a bill to fine tune TABOR.

Two Colorado Republican lawmakers are delivering on their promise from earlier this year to fine-tune TABOR, a 25-year-old constitutional restriction on how much the state can receive — and spend — without triggering tax refunds.

Rep. Dan Thurlow and Sen. Larry Crowder have introduced House Bill 17-1187 that seeks to change the way annual revenue limits set by the 1992 Taxpayer’s Bill of Rights are calculated.

It’s a first step that could allow the state to keep millions of dollars for roads, education and other priorities, starting with an extra $175 million in the 2018-2019 fiscal year, according to legislative analysts.

Thurlow, of Grand Junction, and Crowder, of Alamosa, have asked: What’s the use of individual taxpayer refunds amounting to pocket change when, this year alone, lawmakers must close a $500 million gap to balance the budget that begins July 1?

“I believe our party is the party of solutions and this bill is an example of that,” Thurlow said Monday. Continue reading

The legal battle between an organization representing Colorado small businesses and the Secretary of State isn’t over, despite a Colorado Court of Appeals ruling this week.

“It’s a jump ball,” said Tony Gagliardi, the Colorado director of the National Federation of Independent Businesses, who sued the state of behalf of its members.

The Colorado Court of Appeals this week said the business licensing charges collected by the Secretary of State and used to pay for all the activities run by the office are constitutional under that Taxpayer’s Bill of Rights (TABOR).

But the court ordered the case back to district court and instructed the Secretary of State to produce a list of all the business fee increases since 1992, when TABOR was enacted. Continue reading

What is House Bill 1187?

HB1187 would allow the government budgets at all levels to grow much larger each year by changing the current growth formula of the Taxpayer’s Bill of Rights. The current automatic increase uses the previous year’s budget and adds the growth in population plus inflation.[1] Under the existing formula, Colorado’s State budget has grown an average of 4.7 percent a year for the past 25 years that TABOR has been in effect.

The new formula would replace the growth rate with the growth in personal income, averaged over five years. With that substitution, the TABOR limit would soar.

The measure is sponsored by Rep. Dan Thurlow (R-Grand Junction) and Sen. Larry Crowder (R-Alamosa County).

A fatal flaw in the proposal.

This bill is a very sneaky effort to avoid the constitutional rules altogether. The rules say that the state constitution cannot be changed by passing a law. This proposed measure says it can change a foundational definition in the constitution with a new law. It does not ask simply for the state to keep the excess of taxes collected for some number of years. It is a permanent change in how each TABOR limit is set. That’s a fundamental change to the constitution. Continue reading

Douglas Bruce, author of the state’s Taxpayer’s Bill of Rights, is pictured in 2005 working on the campaign against Referendum C .

By Penn R. Pfiffner and Douglas Bruce | Guest Commentary

PUBLISHED: February 24, 2017 at 1:01 pm

The Taxpayer’s Bill of Rights works for you and its 25th anniversary this year is worth celebrating. Once again in 2017 you need to protect TABOR from the political elite attacking it.

TABOR belongs to you. It is how you set a broad control on government that must answer to you and your fellow citizens. It has succeeded in keeping a better balance between costly government programs and healthy family budgets.

Everyone has to live within a budget. That’s just life. Staying in budget brings stability to your family and helps you choose the most important ways to spend your money. The value of living within a budget applies not just to individuals and families, but also to government. That’s just smart — and fair.

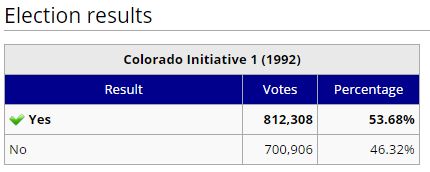

The Colorado Taxpayer Bill of Rights (TABOR), also known as Initiative 1, was on the November 3, 1992 ballot in Colorado as an initiated constitutional amendment, where it was approved. The famed measure, thought up by Douglas Bruce, requires statewide voter approval of tax increases that exceed an index created by combining inflation and population increases.

See also: Colorado State Constitution, Article X

The language appeared on the ballot as:[2]

| “ | Shall there be an amendment to the Colorado Constitution to require voter approval for certain state and local government tax revenue increases and debt; to restrict property, income, and other taxes; to limit the rate of increase in state and local government spending; to allow additional initiative and referendum elections; and to provide for the mailing of information to registered voters? | ” |

See also: Kerr v. Hickenlooper

A lawsuit regarding Initiative 1 will likely have far reaching effects for other TABOR laws around the country and direct democracy, in general. A lawsuit was filed with U.S. District Court in Denver, with plaintiffs arguing that the amendment is unconstitutional. The lawsuit was filed during the week of May 27, 2011, by 34 bipartisan plaintiffs, according to reports.

According to Doug Bruce, author of the citizen initiative, if the lawsuit is successful in its efforts, it could allow lawmakers unlimited power, and could be extremely detrimental to citizen initiative efforts in the state of Colorado. Bruce stated: “This isn’t only attacking Colorado. The consequences of a ruling in their favor would invalidate the Constitution in all 50 states, and would also mean no limits on the federal government. We would have anarchy.”

However, one of the attorneys for the plaintiffs, David Skaggs, stated that the measure limits state legislators and conflicts with both the state and United States constitutions. Skaggs also argues that other initiatives have been overturned, but that it did not negatively affect the process. Skaggs commented: “Courts won’t reach beyond the narrow question presented. Yes, we got to this issue by initiative”, but the lawsuit targets TABOR and not citizens’ initiatives.

The case’s impact expanded significantly due to the consideration of a Guarantee Clause argument. In 2012, Colorado District Court Judge William J. Martínez ruled in favor of allowing the case to proceed. However, Martínez’s ruling noted the history of seeing the Guarantee Clause as not justiciable or capable of judicial resolution, and said, “the Court determines that it cannot summarily conclude that Plaintiffs’ Guarantee Clause claim is per se non-justiciable”

The defense appealed the decision to the 10th Circuit Court of Appeals. In March 2014, the court ruled that the case was justiciable. The court further denied a petition for rehearing en banc in July 2014. Some consider the case likely to reach the U.S. Supreme Court.

http://ballotpedia.org/Colorado_Taxpayer_Bill_of_Rights,_Initiative_1_(1992)

If a person wants to build a single-family home within the Pagosa Springs town limits, he or she must pay $3,342 in Town “impact fees.” That money is purportedly earmarked for the “impacts” that the new residents — who will occupy this new house — will have on roads, recreation facilities, public buildings, parks, trails, emergency services and schools. (Assuming that the people who will occupy this new house haven’t already lived in Pagosa for maybe 25 years.)

The justification typically offered for such fees, is: “growth must pay for growth.”

We are working, here, under the assumption that there is a difference between a “tax” and a “fee.” The Colorado Constitution specifically requires voter approval for tax increases, and for the creation of a new tax — but no such voter approval is required for fee increases, or for the creation of a new fee.

Obviously, the difference is of some significance, here in Colorado.

A recent Colorado lawsuit can help us understand how one particular panel of judges defined the difference between a “tax” and a “fee.”

In 2009, during a particularly difficult period in the financial life of the Colorado state government, the state legislature created a new government agency called the Colorado Bridge Enterprise (CBE). The agency began charging a new “fee” as part of your vehicle registration fee; the money was (purportedly) to be used for repairing state-maintained bridges. The state did not seek voter approval for the new surcharge.

In 2012, the TABOR Foundation filed a lawsuit against the state, arguing that the “fee” was in fact a “tax” — and was thus prohibited by the state’s Taxpayer Bill of Rights (TABOR) unless approved by the state’s voters. During the deliberations, the Colorado Court of Appeals disagreed with one of the TABOR Foundation’s arguments: that the surcharge is a “tax” because it is collected without regard to any services used by the vehicles for which the charge is imposed.

The court laid out three factors that it weighed in determining whether a surcharge is a tax or a fee:

Text of Section 20:The Taxpayer’s Bill of Rights(1) General provisions. This section takes effect December 31, 1992 or as stated. Its preferred interpretation shall reasonably restrain most the growth of government. All provisions are self-executing and severable and supersede conflicting state constitutional, state statutory, charter, or other state or local provisions. Other limits on district revenue, spending, and debt may be weakened only by future voter approval. Individual or class action enforcement suits may be filed and shall have the highest civil priority of resolution. Successful plaintiffs are allowed costs and reasonable attorney fees, but a district is not unless a suit against it be ruled frivolous. Revenue collected, kept, or spent illegally since four full fiscal years before a suit is filed shall be refunded with 10% annual simple interest from the initial conduct. Subject to judicial review, districts may use any reasonable method for refunds under this section, including temporary tax credits or rate reductions. Refunds need not be proportional when prior payments are impractical to identify or return. When annual district revenue is less than annual payments on general obligation bonds, pensions, and final court judgments, (4) (a) and (7) shall be suspended to provide for the deficiency. (2) Term definitions. Within this section:

(3) Election provisions.

(4) Required elections. Starting November 4, 1992, districts must have voter approval in advance for:

(5) Emergency reserves. To use for declared emergencies only, each district shall reserve for 1993 1% or more, for 1994 2% or more, and for all later years 3% or more of its fiscal year spending excluding bonded debt service. Unused reserves apply to the next year’s reserve. (6) Emergency taxes. This subsection grants no new taxing power. Emergency property taxes are prohibited. Emergency tax revenue is excluded for purposes of (3) (c) and (7), even if later ratified by voters. Emergency taxes shall also meet all of the following conditions:

(7) Spending limits.

(8) Revenue limits.

(9) State mandates. Except for public education through grade 12 or as required of a local district by federal law, a local district may reduce or end its subsidy to any program delegated to it by the general assembly for administration. For current programs, the state may require 90 days notice and that the adjustment occur in a maximum of three equal annual installments.[1] |