Most Coloradans won’t get a TABOR tax refund next spring even though the state collected millions more dollars than it’s allowed to keep, according to the quarterly revenue forecast presented to lawmakers Thursday.

The Taxpayer Bill of Rights, or TABOR, limits how much money Colorado can collect from residents each year. Whatever comes in above the limit has to go back to the people. And for the fiscal year that ended in June, that’s a total of about $37 million.

However, a 2017 law requires the first refunds go to the state-administered senior homestead exemption and disabled veterans property tax exemption before they go to everyone else.

Exceeding the TABOR limit is a sign of the Colorado economy’s continued growth — even beyond the expectations of just a few months ago. In the last quarterly report, in June, state forecasters thought revenue would come in under the TABOR cap by $93 million.

Carol Skubic, secretary and treasure, left, and Sharon Raggio, CEO of Mind Springs Health and West Springs Hospital, right, answer questions about the county’s proposed TABOR exemption outside the West Springs Hospital on Tuesday.

Chancey Bush

A ballot measure that would allow Mesa County to accept state grants as a revenue stream outside strict governmental growth limits could open potential funding sources for local projects, ranging from a psychiatric hospital facility to a new space for a nonprofit that services developmentally disabled adults, advocates said at a Tuesday press conference.

Leaders of Mind Springs Health, the Grand Junction Area Chamber of Commerce and other local organizations called the event Tuesday morning, the day after the Mesa County Commission voted to place Issue 1A on the November ballot.

The ballot issue involves Mesa County’s relationship with the Taxpayer’s Bill of Rights, which limits governmental income, including grants, unless an exception is made. Mesa County voters in November will decide whether the county can permanently make that exception for state grants, which are often applied for by nonprofits using the county government as a pass-through agency.

The still-under-construction Mind Springs Health psychiatric hospital project became a case study on the legal tangle last year when the county decided not to apply for a $5 million grant that could have made a major dent in the group’s fundraising goals in anticipation of going over TABOR limits.

“Had we been able to partner with the county as well as other communities in being able to secure some TABOR funds, that would have really put us over the top (of fundraising efforts),” said Mind Springs President and CEO Sharon Raggio at the event outside the facility.

HopeWest President and CEO Christy Whitney said she hopes voters will agree.

“There’s a lot of state money available to make some amazing things happen in Mesa County, but we have just fundamentally not been able to access it because of the really outdated view of the TABOR law,” Whitney said.

Diane Schwenke, president and CEO of the Grand Junction Area Chamber of Commerce, said both her organization and the Grand Junction Economic Partnership are behind the measure, in part because they believe that local nonprofits provide important services that serve the workforce, that the ballot measure is in “the spirit”of TABOR, and that state grants are partially funded by severance taxes that local businesses pay.

“It’s only right that those dollars can come back and help the nonprofits that are doing the good work,” Schwenke said.

The PVFPD stands to lose at least $860,000 per year, on an ongoing basis starting in 2020.

Poudre Fire Authority Logo

Madeline Noblett, Public Affairs and Communication Manager

Residents and owners of property within the Poudre Valley Fire Protection District are invited to two upcoming public meetings at which officials will provide information about a possible ballot question voters may be asked to consider for November’s mid-term election.

The meetings are 6:30 to 7:30 p.m. and open to the public. The first meeting is Aug. 30 in Laporte at Station 7, 2817 N. Overland Trail. The second meeting is Sept. 4 in Timnath at Station 8, 4800 Signal Tree Drive, in the station’s community room. There is no need to RSVP.

The Poudre Valley Fire Protection District Board is considering a ballot question that would ask district residents and property owners to annually adjust the District-assessed mill levy – a term referring to the property tax rate – so the district may maintain its current level of funding. City of Fort Collins residents would not vote on the possible question.

The Poudre Valley Fire Protection District, or PVFPD, encompasses the Town of Timnath, the communities of Laporte and Bellvue, Horsetooth Reservoir, Redstone Canyon, and areas of unincorporated Larimer and Weld counties. Poudre Fire Authority was established in 1981 through an Intergovernmental Agreement between the PVFPD and the City of Fort Collins. Simply put, PFA’s firefighters provide services to people within Fort Collins and the PVFPD.

Because of a collision between the Gallagher Amendment and the Taxpayer Bill of Rights, or TABOR, the PVFPD stands to lose at least $860,000 per year, on an ongoing basis starting in 2020. At this time, the PVFPD can’t specify how this would impact the District; that’s ultimately up to the PVFPD Board to decide. However, board members would likely have to consider a range of options that could include closing a fire station or eliminating positions. To learn more about the intersection of TABOR and Gallagher, watch this video from the nonprofit non-partisan Colorado Fiscal Institute: http://youtu.be/BXbrsdQQrZ8

Approved in 1992, TABOR demands that Colorado voters approve all tax increases. The Gallagher Amendment stipulates that residential property taxes are capped at 45 percent of the state’s total property tax revenue, while non-residential property taxes comprise the other 55 percent. Non-residential property is taxed at 29 percent of its value. Residential property is currently taxed at 7.2 percent, but the residential rate can fluctuate to maintain the 45-55 split. It may go down to 6.11 percent, which could lead to the loss in revenue for the PVFPD.

With the state of Colorado expected to generate about $1 billion in new state revenue in fiscal 2020, state law may require that the state refund roughly $148 million to taxpayers.

The Economic and Revenue Forecast presented to the Joint Budget Committee in June showed that the state’s general fund is projected to close out fiscal 2018 with a $1.2 billion surplus.

Since Colorado’s Taxpayer’s Bill of Rights (TABOR) places a cap on annual state tax revenue the state can keep, spend or save, many wonder whether Coloradans will actually see tax refunds in 2020.

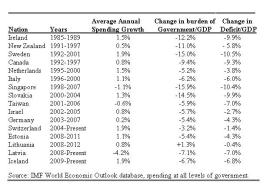

The best budget rule in the United States is Colorado’s Taxpayer Bill of Rights. Known as TABOR, this provision in the state’s constitution says revenues can’t grow faster than population plus inflation. Any revenue greater than that amount must be returned to taxpayers.

Combined with the state’s requirement for a balanced budget, this means Colorado has a de facto spending cap (similar to what exists in Switzerland and Hong Kong).

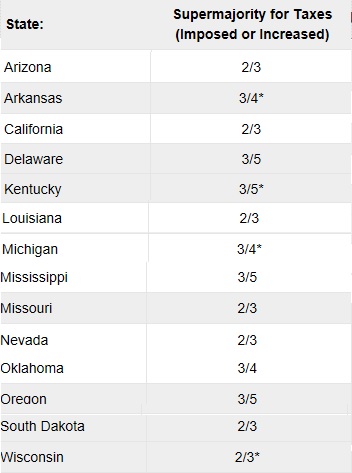

The second-best budget rule is probably a requirement that tax increases can’t be imposed without a supermajority vote by the legislature.

The underlying theory is very simple. It won’t be easy for politicians to increase the burden of government spending if they can’t also raise taxes. Particularly since states generally have some form of rule requiring a balanced budget.

If you want proof for that assertion, check out states such as Illinois, California, and New Jersey. They all have provisions to limit red ink, yet there is more spending (and more debt) every year. There are also anti-deficit rules in nations such as Greece, France, and Italy, and those countries are not exactly paragons of fiscal discipline.

That’s why I’m a big fan of the “debt brake” in Switzerland’s constitution and Article 107 in Hong Kong’s constitution.

And it’s also why the 49 other states, assuming they want an effective fiscal rule, should look at Colorado’s Taxpayer Bill of Rights (TABOR) as a role model.

Colorado’s Independence Institute has a very informative study on how TABOR works and the degree to which it has been effective. Here’s a good description of the system.

Colorado voters adopted The Taxpayer’s Bill of Rights in 1992. TABOR allows government spending to grow each year at the rate of inflation-plus-population. Government can increase faster whenever voters consent. Likewise, tax rates can be increased whenever voters consent. …The Taxpayer’s Bill of Rights requires that excess government revenues be refunded to taxpayers, unless taxpayers vote to let the government keep the revenue.

And here are the headline results.

Cumulatively, TABOR refunds have been over $800 per Coloradan, or $3,200 for a family of four. …If Colorado government had continued growing at the same high rate (8.56% compound annual rate) as in 1983-92, the average Coloradan would have paid an additional $442 taxes in 2012. The cumulative two-decade savings per Coloradan are $6,173—or more than $24,000 for a family of four.

Opinion: Newcomers need to know benefits of Colorado’s Taxpayer’s Bill of Rights

Jennifer Schubert-Akin and Amy Oliver Cooke

For Steamboat Pilot & Today

The latest Census Bureau data released earlier this year shows that Colorado’s population has grown by nearly two-thirds since 1992, one of the fastest increases in the country.

If you are part of the more than two million new residents who have arrived over this time, there are a few things you should know: Avoid I-70 on Sundays. We are Coloradans, not Coloradoans. And the Taxpayer’s Bill of Rights is responsible for much of the state’s economic success, which likely drew you here in the first place.

Between 1992 and 2016, median household income in Colorado grew by 30 percent, adjusted for inflation. This growth was more than double the national rate over the same period. Only Minnesota and North Dakota grew by more than 30 percent over this timeframe. Colorado gained $20 billion in adjusted gross income over these years — again, one of the biggest increases in the nation.

While many other states have struggled with stagnant incomes over this period, what’s set Colorado apart? Its Taxpayer’s Bill of Rights, or TABOR, passed in 1992, which requires state and local governments to ask voters for permission before raising taxes or debt.

TABOR helped end years of economic stagnation and laid the groundwork for the state’s future success by keeping resources in the hands of Colorado residents who could put them to their highest valued use and checking overzealous government spending.

TABOR has protected pocketbooks and state solvency from legislators who believe they know how to spend your money better than you. Its requirement that excess revenues must be refunded to taxpayers has also resulted in more than $2 billion being returned to the private economy to be spent at local businesses or saved for retirement.

Editor’s Note: Denver7 360 stories explore multiple sides of the topics that matter most to Coloradans, bringing in different perspectives so you can make up your own mind about the issues. To comment on this or other 360 stories, email us at 360@TheDenverChannel.com. See more 360 stories here.

DENVER — Whether you’ve lived in Colorado for a short time, or your entire life, you’ve probably heard about what’s known as TABOR: The Taxpayer’s Bill of Rights.

Promoted by Republican lawmaker Douglas Bruce, voters in Colorado passed it back in 1992. Under the TABOR amendment, taxes can’t be raised without voter approval. That includes the state sales tax and property taxes.

“It ensures that government cannot grow beyond what the people want it to do,” said Michael Fields of the conservative-leaning group Americans for Prosperity.

Fields argues TABOR leads to smart spending with an existing budget, prevents government from getting out of control and gives people of Colorado the power to decide when it’s appropriate to raise taxes.

“I think you make the case to the people,” Fields said. “If you want to invest in something more, then go make the case to the people – convince them that they need more revenue and that’ll pass.”

But there’s another side to TABOR.

“It’s not something good to have on our books. It’s actually hindered our ability as a state to do many things,” said TABOR opponent Amie Baca-Oehlert, of the Colorado Education Association.

She says she feels TABOR is a roadblock for lawmakers that prevents them from making responsible spending decisions in places where it is needed most, like Colorado’s schools.

“That just doesn’t seem right in a state with such a fast-growing economy,” she said.

But Colorado needs money to fix our ailing roads and bridges. So a push is underway to convince voters to approve a sales tax hike this November. Educators are also pushing a tax increase to help public schools after a 2013 $1 billion proposed tax increase to pay for school funding was rejected by voters.

On Monday, the Colorado Supreme Court ruled that an Aspen grocery bag surcharge was not a tax and thus did not fall under TABOR – the second successful challenge in recent months.

But what’s next? For the moment TABOR is here to stay. In order for it to be reversed completely – we as Coloradans would have vote to change it.

Colorado Supreme Courtroom in the Ralph L. Carr Colorado Judicial Center

Nagel Photography | Shutterstock.com

Over the last 25 years, the Colorado courts have consistently legislated from the bench to weaken the state’s Taxpayer Bill of Rights (TABOR), two prominent advocacy groups committed to limited government assert. A recent Colorado Supreme Court ruling is one among many that “weakened taxpayer’s rights,” they argue.

Voters approved TABOR on Nov. 3, 1992, which then became part of the state constitution after the governor issued a proclamation on Jan. 14, 1993.

TABOR requires voter approval of most tax and debt increases. It also requires each government to reserve a percentage of non-debt-service spending (an amount that has fluctuated) for emergency reserves. It states that TABOR “shall reasonably restrain most of the growth of government. All provisions are self-executing and severable and supersede conflicting state constitutional, state statutory, charter, or other state or local provisions.” Continue reading →

The topics that will dominate candidates’ messaging throughout the campaign season.

Growth

It is the best of times…or is it the worst of times? That depends a lot on how you feel about Colorado’s growth. “Normally, the economy would be the highest issue for most voters,” Paul Teske, a dean at CU Denver, says. “There will be a lot of talk about sustaining the boom.” But, adds DU’s Seth Masket: “There are a lot of different areas of the state that are adversely affected by this growth.” Transportation has become a perennial funding battle at the Capitol and could benefit from strong gubernatorial influence (read: political pressure) to make Republicans and Democrats find bipartisan ways forward. Meanwhile, the unemployment rate in Colorado is three percent (it was 8.9 percent at the end of 2010), which on its face is great news, but that near-full employment causes woes for companies desperate to fill jobs. Wages—particularly in the metro area—haven’t kept up with cost-of-living expenses, which means that although people are finding work, they may not be able to pay bills. And the biggest expense for many voters is rising housing costs. Mix that all together, and the moment is prime for a gubernatorial candidate to stand out by creating a unique vision for Colorado’s future.

Education

This may seem like a topic that matters most to people who are raising families, but this year, candidates will compel everyone to think about Colorado’s education system (funding here ranks in the bottom third of all states in the country). Which makes sense: Property owners help pay for schools, employers benefit from a well-prepared workforce, and we all want the best for society’s youngsters, right? But how we ensure we have a strong education system is quite a bit more complicated. Magellan Strategies’ David Flaherty says Republican candidates should be talking about education right now and through November. “It’s the one issue we completely give to the Democrats,” Flaherty says. “It’s unfortunate because it’s one of the top two issues for unaffiliated voters.”

Tabor

Conversations about addressing growing pains or giving more money to teachers inevitably evolve into talks about what to do about Colorado’s Taxpayer Bill of Rights (TABOR), which limits government spending to match population growth and inflation increases.

Under TABOR, which passed in 1992, leftover revenue is returned to the taxpayers. Proponents herald the limits on government spending; detractors warn that TABOR isn’t robust enough to respond to real-time needs, like shifting populations in schools due to high housing costs.

But Coloradans tend to like the control TABOR gives them: A January 2018 report from the American Politics Research Lab at CU Boulder found that “support among Coloradans outpaces opposition,” with 45 percent of respondents supporting TABOR.

That number has fallen since 2016, and the study notes that more than a quarter of respondents had “uncertainty about a position.” In short, there’s room for candidates to make TABOR the issue of the campaign.

Republican candidates are likely to support working within TABOR’s constraints. Democrats will probably talk more about reform or repeal.

Editor’s Note: Denver7 360 stories explore multiple sides of the topics that matter most to Coloradans, bringing in different perspectives so you can make up your own mind about the issues. To comment on this or other 360 stories, email us at

Editor’s Note: Denver7 360 stories explore multiple sides of the topics that matter most to Coloradans, bringing in different perspectives so you can make up your own mind about the issues. To comment on this or other 360 stories, email us at