May

15

Category Archives: Editorial

May

14

Lewis: A wolf in sheep’s clothing

Lewis: A wolf in sheep’s clothing

Colorado’s Taxpayer Bill of Rights, approved by voters in 1992, was intended to limit the tax revenue that the state government can retain for spending ensuring that government spending doesn’t spiral out of control. However, it seems that a cunning wolf is attempting to enter the flock.

Prior to 2022, TABOR refunds were tiered based on the amount taxpayers paid. The more you paid in taxes, the higher refund you received. However, last year, Gov. Polis and the Democrats accelerated the refund process and sent out identical amounts to everyone, regardless of their actual tax payments. At the time it seemed innocuous, but now I’m not so sure.

As homeowners, many of us have just received our new property valuations. While I’m happy that my home value has increased dramatically, the thought of my new impending tax bill sent chills down my spine. The prospect of my taxes nearly doubling made me cringe. Fortunately, Colorado has a provision that limits property tax revenue increases to 5.5% so hopefully, the blow won’t be too severe.

Recently, the Colorado legislature passed a proposal to “lower” property tax rates, which sounds promising. However, upon closer examination, it’s apparent that this proposal is a wolf in sheep’s clothing. Rather than reducing taxes, it merely restricts increases while diverting money from our TABOR refunds to more than cover any revenue loss. Moreover, an attached provision effectively establishes a state-administrated welfare system funded by TABOR dollars. Talk about deceiving the flock.

Allow me to break it down for you. The property tax reduction proposition (Proposition HH) includes a provision to fund any loss of revenue from the general fund. Essentially, it’s a shell game. While the proposal claims to lower taxes, the net result is zero savings for taxpayers. Additionally, while it mandates limits on assessment rates, that actually won’t necessarily curb taxes since municipalities remain free to adjust their levies. There is a limit on tax revenue increases but, with today’s inflation, that limit would be higher than the existing 5.5% limit in place today. It’s like chasing your tail, going in circles with no progress.

Within this proposition, there is a second provision (HB 23-1311) regarding TABOR refunds, which would change the refund method to the single fixed value payout (as used in 2022) regardless of taxpayers’ actual contributions. Interestingly, this provision passes automatically if voters approve the property tax proposition. The reason behind connecting these two provisions is a mystery. It appears like a wolf is trying to sneak into the flock.

State Senate Majority Leader Dominick Moreno argues for equal distribution claiming that a tiered rebate system is not “equitable,” and that the money should go to those with the most need. But let’s pause for a moment. TABOR is not a welfare program — it is a tax refund program.

When it comes to refunds, rebates, or dividends, the amount you receive is typically based on your investment. If you’re a stockholder, the dividend you get depends on the number of shares you own. It’s straightforward. If you tax people based on their income and then rebate them a flat amount, it is no longer a taxpayer bill of rights — it’s a welfare program in disguise. In this case, an 18-year-old kid who plays video games all day in the basement of his parent’s house would get the same “rebate” as the parent who works 60-hour weeks and pays thousands in taxes. Is that truly equitable?

We strive for a society that strikes a balance between capitalism and socialism, supporting those in need while motivating everyone to work hard and enjoy the fruits of their labor. We already have various programs to aid those in need and always have the option to create more, but transforming TABOR into a socialistic welfare program administered by the state is disingenuous as that was never its intended purpose.

So, it all becomes clear now. There is a proposition to lower property taxes which most people will likely vote for, believing it will provide relief. The only problem is that it doesn’t actually lower taxes. I am going to dig into this further, but I actually think this bill could actually significantly increase taxes. Meanwhile, a hidden second proposition, covertly transforms a tax rebate program into a social welfare program, effectively turning TABOR into a new tax on higher-income residents. That is one sneaky wolf.

Mark Lewis, a Colorado native, had a long career in technology, including serving as the CEO of several tech companies. He retired from technology and is now writing thriller novels. Mark and his wife, Lisa, and their two Australian Shepherds — Kismet and Cowboy, reside in Edwards.

https://www.vaildaily.com/opinion/lewis-a-wolf-in-sheeps-clothing/

#DontBeFooled

#ItsYourMoneyNotTheirs

#VoteOnTaxesAndFees

#FeesAreTaxes

#TABOR

#ThankGodForTABOR

#FollowTheMoney

#FollowTheLaw

May

01

Twitter Post By Roger D. Hudson About TABOR, Gov. Polis, & Colorado’s Property Tax Problem

Roger D. Hudson @RogerHudsonCO

Polis unveiled his plan to fix Colorado’s #PropertyTax problem — it asks voters to use TABOR refunds. “While we at the Capitol were making new laws that were too expensive, real Coloradans have been opening up their mail —finding tax bills they can’t pay. bit.ly/3B2zDSd

May

01

TABOR Gives Taxpayers a Voice

TABOR Gives Taxpayers a Voice

By Dennis Polhill

By Dennis Polhill

A recent election result showed the great value of the requirement within the Taxpayer’s Bill of Rights for voters to approve new taxes or debt. There was a TABOR election in the Foothills Fire Protection District (FFPS). The outcomes measure how upset voters were with the proposed actions of elected officials.

Ballot issue 6B would have allowed the District to issue new debt. That was soundly defeated 74.11% to 25.89%

Ballot issue 6C would have increased taxes and it too was defeated, by 66.98% to 33.02%

The tactics used to obtain this taxpayer money were very questionable. A former board member who painstakingly reviewed all meeting documentation learned that there had been absolutely zero public discussion of the proposed ballot measures prior to the August meeting when the measure was placed on the ballot. Yet, the proposal passed unanimously – without discussion! Had something been happening behind the scenes, in violation of the Sunshine laws? Note that the August meeting was the last possible moment to meet the County Clerk’s deadline for a November citizen vote to put the referral to the ballot .

Paradise Hills Homeowners Association on Lookout Mountain accounts for close to half of the homes protected by FFPD and owns a vacant lot designated for open space use near an I-70 highway exit. At a Homeowners Association meeting an alert retired firefighter picked up on what was happening when it was mentioned that FFPD would buy the vacant lot for a new station for $400,000, yielding a significant rainy day fund or dues waiver for Homeowners Association owners. Did FFPD intend to buy their votes with their own tax dollars?

Citizens immediately started getting the word out; flyers were printed, yard signs went up, and a couple of large banners created. Comments on Nextdoor were not friendly to FFPD, resulting in the censoring from Nextdoor of some neighbors who posted information.

By this time the community was in angry uproar and five folks who otherwise likely would never have run for any office are now candidates for the five seats on the FFPD board due to be elected on May 2, 2023.

![]()

Mar

17

Bullet Point #1 Under Taxation In The Colorado Democrat Party Platform

Did you know?

The Colorado Democrat’s party platform states that they want to eliminate TABOR?

Mar

17

Will The Left Abolish TABOR?

Friday @CompleteCO update:

@JonCaldara, @MichaelCLFields and @benamurrey on defending and strengthening the Taxpayer’s Bill of Rights

#copolitics

http://CompleteColorado.com

https://twitter.com/CompleteCO/status/1636728225970946048?s=20

Click this link, https://www.youtube.com/watch?v=gGkh2Kg-MJU, to watch Jon Caldara, Michael Fields, and Ben Murrey discuss TABOR;

Mar

09

Americans For Prosperity Supports the Taxpayer’s Bill of Rights

TABOR supporter,

Did you know Americans For Prosperity has been promoting and protecting TABOR, the Taxpayer’s Bill of Rights?

Attached is a brochure with their latest activities.

You can learn more by checking their website, https://americansforprosperity.org/state/colorado/

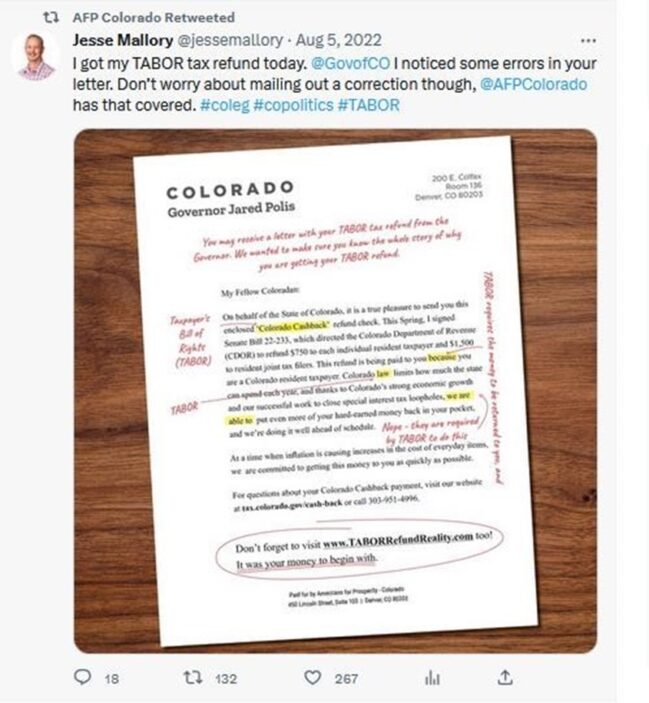

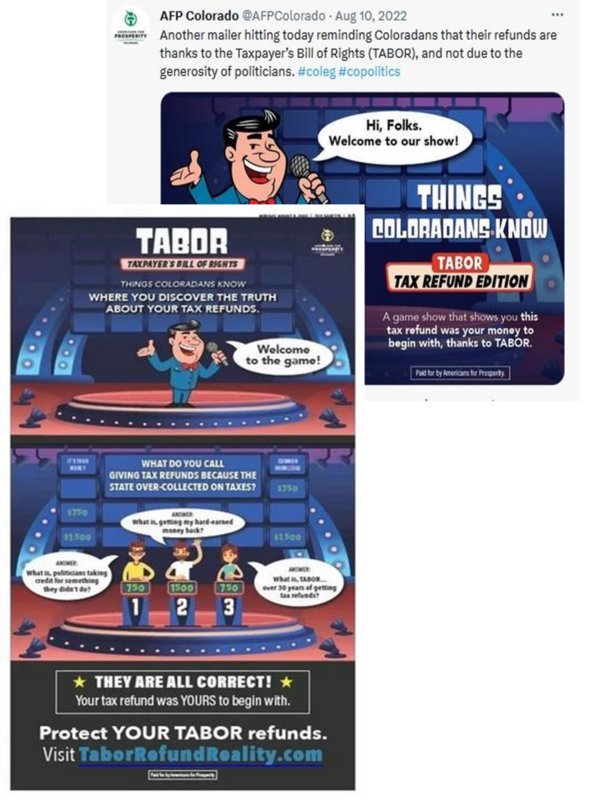

The purpose of this letter is to share a list of Americans for Prosperity’s vigorous activities educating the public about TABOR over the last several months.

Since not everyone may have witnessed those efforts (much is visible on facebook and twitter), I’m including some social blurbs and photos. These blurbs just span back to the July-August 2022 period and I certainly haven’t included all their activities, though there’s more available.

AFP mailers to voters that refunds were thanks to TABOR.

Then, AFP engaged in a gas promotion with unleaded at $2.38 per gallon. AFP covered the difference between the $2.38 and the going rate of $4.45. While drivers waited in line to get the promo gas price, AFP shared information about the Taxpayer’s Bill of Rights, handed out promo materials and water. Continue reading

Mar

06

TABOR: Taxpayer’s Bill of Rights

#DontBeFooled

#ItsYourMoneyNotTheirs

#VoteOnTaxesAndFees

#FeesAreTaxes

#TABOR

#ThankGodForTABOR

#FollowTheMoney

#FollowTheLaw

Feb

22

Menten: How to get involved in the May special district elections

Menten: How to get involved in the May special district elections

February 21, 2023 By Natalie Menten

There are over 4,500 local government agencies in Colorado. Nearly 3,000 of those are special districts. All of these agencies and special districts are included under our Taxpayer’s Bill of Rights (TABOR).

Most voters wouldn’t be able to list off the top of their head all the local governments collecting property taxes from them either directly, or passed on to them as a percentage of rent by the property owner in the course of business. You might have a couple or even several of these governments charging you property taxes — lots of layers.

You can check your special districts using this Colorado Department of Local Affairs (DOLA) GIS map. It’s a great tool offering filters and layers so you get all the information. Click on the district map and you’ll get the annual levy rate and contact information for the district.

Why should you care?

Special districts, especially metropolitan districts, can amount to a sizable portion of your property tax bill. Just because you don’t directly write the check for the property taxes doesn’t mean you’re not footing part or all of the property tax tab. Tenants and consumers pay a portion of the property taxes in rent or included in the cost of the products they buy.

Some special districts, especially metropolitan districts, may rival the mill levy rate or dollar amount of school district property taxes — usually the most expensive item on your property tax bill.

The list of all Colorado Property Tax Entities 2022 Mill Levy Rates is found here. Some are nearly 100 mills! Continue reading

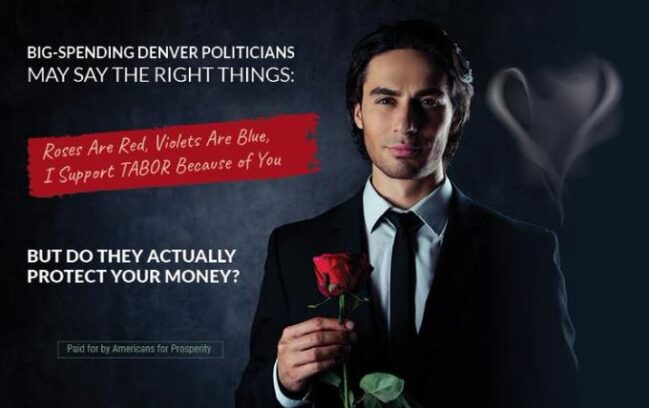

Feb

15

Americans For Prosperity’s Valentine’s Day Card To Colorado

AFP Colorado@AFPColorado

ICYMI: A valentine mailer that hit across Colorado reminding voters to pay attention to an elected official’s actions and not just their words when it comes to the Taxpayer’s Bill of Rights (TABOR)