Colorado voters will be asked in November to vote on Proposition HH. As with most ballot measures, it is written to sound very good and appealing. It starts out, “Shall the State reduce property taxes….” And, of course, like most ballot measures, that’s misleading and the actual text of the measure is complex.

You will, and are already, seeing social media posts and news coverage, and have probably received the first of many mail pieces about Proposition HH. You will be bombarded with numbers and formulas and forecasts. One such piece, designed to “simplify” the measure included the following dollar amounts – in just one piece: $1,074 million; $620 million; $2 billion; $145 million; $72 million; $287 million; $3.5 billion; $21 million; $94.3 million; $2.2 billion; $128 million; $161.3 million; $278 million; $351 million.

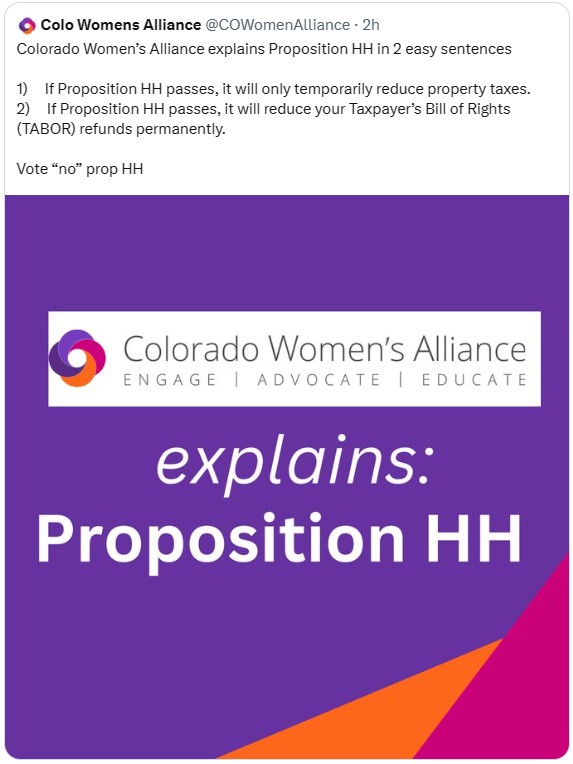

So, here’s what it all boils down to. Here are the two sentences that you need to know when you vote your ballot this fall:

1) If Proposition HH passes, it will only temporarily reduce property taxes.

2) If Proposition HH passes, it will reduce your Taxpayer’s Bill of Rights (TABOR) refunds permanently.

That’s it. All that mumbo jumbo, simply explained in two sentences.

Property owners – your property taxes will still go up, just not as drastically, for a limited time.

Renters – your rent will still go up, because your landlord needs to recoup the increase in taxes.

Everybody – your TABOR refunds (remember those $750 or $1,500 checks?) will permanently be decreased and, because of a change in formula, eventually will go away forever.

The Colorado Women’s Alliance urges you to remember those two simple sentences when it comes time to mark your ballots. Vote “no” on Proposition HH.

Many, many thanks for dealing with my City Clerk and Attorney on Thursday, the day before the TABOR con statement noon deadline.

I called the City Clerk mid-Thursday-morning to confirm that the TABOR Con Statement deadline was noon the next day. The City Clerk firmly informed me that City Ballot issue 3K did not warrant TABOR statements. I was incredulous, but reluctantly listened. I politely hung up and promptly called Natalie Menten, who got Sherrie Peif, an investigative reporter, to call the city clerk and city attorney. THREE hours later the City Clerk called me to apologize for having given me incorrect advice. We agreed that the deadline was the next day and 3K was a TABOR issue. The next day I submitted a con statement; thanks to all you’ve done!

Again, thanks; your TABOR Foundation expertise got the CON statement published.

GUEST COLUMN: Thanks to TABOR, Colorado works for everyone

Jesse Mallory

Aug 27, 2023

Legislative Democrats have been scheming to kill Colorado’s Taxpayer’s Bill of Rights, or TABOR, since before it was added to the state Constitution in 1992. Hardly a year goes by without a bill, proposal, “listening tour,” or lawsuit hatched to enable state legislators to spend money TABOR denies them. Now, they’re at it again.

This time, they’ve proposed a Rube-Goldberg ballot initiative called Proposition HH. Some of its superficial details might seem novel — like lipstick on the proverbial pig — but it’s only the latest gambit in a political long-con that has gotten very, very old.

That’s why the bill creating Prop HH was only passed in the last hours of the 2023 legislative session — to avoid public scrutiny and debate. That’s why Prop HH’s fans, including Gov. Jared Polis, are so cagey about what it would actually do, talking up property tax relief while pretending to know nothing about the redistribution of TABOR revenue to Democrat priorities.

And it’s why Americans for Prosperity and Americans for Prosperity-Colorado Issue Committee have joined up with more than a dozen citizen groups in a new coalition to protect TABOR and fight Prop HH at the ballot box and in state court this year.

What politicians and their special-interest allies are not telling you about Prop HH is that it will eventually eliminate TABOR refunds.

Those are the same refunds they expedited last year to ensure they arrived before the last election — saying that citizens desperately needed the money.

To add insult to injury, Prop HH will also allow local governments to keep money owed to you without voter approval. Now politicians at the local level can now vote to keep your money. Prop HH removes you from this conversation.

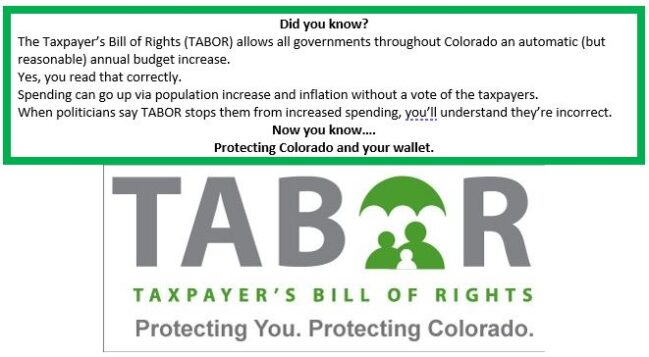

For all the excuses, pretenses, and shiny objects politicians offer up to distract Colorado voters, there is only one reason they want to “update” or “tweak” or “modernize” TABOR: It works at holding them accountable. TABOR limits the annual growth of state government spending to population growth plus inflation. It’s a padlock on the state treasury that big-spending politicians have been trying to pick, break or dynamite for a generation.

Since TABOR was passed, and government spending capped, the state’s economy has consistently outperformed the nation as a whole. Between 1997 and 2022, for instance, Colorado’s real gross domestic product grew 109% while the country’s rose only 73%, increasing our share of national GDP by 18%.

Not surprisingly, TABOR is very popular — garnering 77% support in a 2022 survey. And perhaps even more to the point, since TABOR passed, so many Americans have relocated to Colorado that we’ve gained two seats in the U.S. House of Representatives over the last three censuses.

At a certain point, one has to ask whether Colorado has succeeded so spectacularly over the last three decades in spite of our politicians’ limited control over taxpayers’ money — or because of it.

After all, the big-government states that Democrats want to emulate — New York, California, Illinois — are the ones that new Coloradans escaped here from!

Under TABOR, when the state raises more money in taxes than it is permitted to spend, the money is returned to taxpayers — period, end of story. Under our state Constitution, that money is Coloradans’ right, not doled out at the discretion of politicians or the influence of special interests.

Prop. HH’s sole purpose is to gut that right and seize the cash — not for Colorado, but from it.

Gov. Polis and legislative Democrats are certainly right that the government should take measures to lower the high cost of living in the state. But they’re the ones driving it up! If property taxes are too high, they can cut the rates. If education and health-care programs need reforming, other states — including two of our “Four Corners” neighbors — have shown that market-oriented consumer choice and less government control lower costs and improve quality.

Contrary to the elite narrative, TABOR is not an obstacle to opportunity and prosperity in Colorado; it is a wellspring of both. AFP-Colorado and the new TABOR coalition are going to make that case until politicians remember that they work for us, not the other way around.

Jesse Mallory is state director for Americans for Prosperity-Colorado.

In October 2023, Colorado voters are going to get a ballot information guide, nicknamed the Blue Book (it literally has a blue cover page) in the mail prior to the arrival of their actual ballots.

This year the Blue Book will cover the two statewide tax increases – Proposition II and HH.

Common questions during the election include who phrases the ballot questions and who writes the Blue Book. This is especially true when ballot questions are deceptively worded like Proposition HH, which paints pictures of pies in the sky without disclosing the real intent to screw you out of your Taxpayer’s Bill of Rights (TABOR) refunds for at least the next 10 years, and likely forever.

The Blue Book is where you can make a difference. You get to participate and no expertise is needed. There’s a special reason that you’re especially needed this year.

Slick politicians wrote the Prop HH ballot language and rushed it through the state legislature without responsible notice to the public. A recent survey indicates 2/3 of voters will vote for Proposition HH if they read only the deceptive and misleading ballot question that state Representatives Chris deGruy Kennedy and Mike Weissman, and Senators Steve Fenberg and Chris Hansen cunningly wrote.

It’s up to us to ensure content in the ballot guide provides a full and clear picture to voters. Otherwise, the majority of the players at the table are the very politicians who hate spending limits and TABOR, like the sponsors of Prop HH (Senate Bill 23-303). Continue reading →

David Flaherty is CEO of Magellan Strategies, a CO-based public opinion polling and survey research firm. He recently did an interesting poll about Proposition HH, a measure on this November’s ballot which will slightly lower property tax rates while all but eliminating (over several years) TABOR refunds. It’s a disgusting and cynical ploy which I will work hard to defeat. The poll’s findings are interesting: in short, people like HH until they understand it. The implications are obvious.

ALEC Executive Vice President of Policy and Chief Economist Jonathan Williams discusses an upcoming Colorado ballot measure that would expand government spending and weaken Colorado Taxpayer’s Bill of Rights (TABOR), the nation’s strongest taxpayer protection.

The progressive push to undermine common sense checks on government spending is never-ending. It’s evidenced recently by the debate over the federal debt limit in Washington DC. The latest push is happening in Colorado as progressives are once again attempting to undermine the taxpayers’ Bill of Rights or TABOR, which is the gold standard of a state constitutional limit on overspending and overtaxing. It was adopted by voters as a state constitutional amendment back in 1992. It has helped restrain the growth of government and return billions of dollars to Colorado taxpayers.

However, the upcoming ballot measure in Colorado if approved, would gut TABOR in exchange for small, short-term cuts to property tax. Known as Proposition HH, this proposal tempts voters with the allure of a property tax cut with its real purpose is to clearly to water down TABOR’s tax and spending limits. My friend Ben Murray, Director of fiscal policy at the Independence Institute, described the package as a boondoggle of a property tax plan. The attacks on TABOR aren’t new. The property tax cut quote unquote, is the only latest gimmick to attempt to unleash the leviathan of big government on hardworking Coloradoans.

As the ALEC team explained in the National Review on the recent 30th anniversary of TABOR, TABOR has seen no shortage of progressive attacks which serves as an acknowledgement of the danger it presents to those that would like no constraints on the government’s ability to grow. Though all states except Bernie Sanders of Vermont have some sort of a balanced budget requirements in state law or their constitution, most don’t have robust protections such as that what TABOR offers.

Colorado economic forecasters predict another tax refund windfall next spring — though how Coloradans receive the excess collections depends on how they vote this November.

Forecasters for both the legislative and executive branches expect tax collections subject to Taxpayer’s Bill of Rights, or TABOR, caps to exceed $3.3 billion. That would be near the prior year’s record that lawmakers refunded through direct checks last fall. Following year forecasts still show excess collections, though not nearly as eye-popping.

The excess collections will surely become a point of leverage in a looming ballot box battle over state tax policy. Voters will decide this November on Proposition HH, a multi-faceted proposal aimed to blunt the sharpest edges of rising property taxes while also allowing the state to keep more tax dollars than currently allowed under TABOR.

Opponents are arguing its passage would lead to a long-term vacuuming of tax dollars that would otherwise be returned to taxpayers. Supporters, including Gov. Jared Polis and many lawmakers, argue the measure is necessary to backfill local governments and services whole while saving property owners hundreds of dollars a year in higher taxes driven by skyrocketing property values.

As an additional carrot, lawmakers attached a one-year, flat TABOR refund to the proposal passing. Economic forecasters with the Governor’s Office of State Planning and Budgeting predict individual taxpayers would receive $873 per filer — if HH passes. Forecasters for the legislative branch, who estimate a slightly lower breach of the TABOR cap, predict it would be about $854.

If Proposition HH doesn’t pass, the state would revert to the six-tier refund mechanism that gives lower-income taxpayers lower refund amounts, and higher-income taxpayers higher refunds, under the philosophy that higher-income taxpayers paid more into the overcollected taxes.

We follow the bills as best we can, but do not rate them, relying instead on the excellent and thorough Colorado Union of Taxpayer’s work and that done by others, such as the Republican Liberty Caucus. There were a few good ideas and plenty of bad ones, but we focused only on those that affect TABOR.

The General Assembly pretty much left the Taxpayer’s Bill of Rights alone until the final week of the legislative session. Then, legislators dropped a big negative on Colorado with a bill to place Proposition HH on the ballot this fall.

The entire idea is bad. It is very complex and convoluted legislation that proponents tout as lowering your property taxes. It fails. The Gallagher Amendment was repealed a couple years back. That action removed the method to tamp down increases in residential property taxes. With property taxes threatened to soar next year, Proposition HH (Senate Bill 23-303) takes money owed back to the taxpayer to reduce some (perhaps half) of the property tax increase. It literally uses a big tax increase by taking your TABOR rebates in order to pay down your property tax increases! Dastardly. Sneaky. Terrible.

What is your TABOR Committee doing about it? We brought together like-minded organizations to protect TABOR by defeating this crumby, lose-lose measure, in which only the government benefits. The new coalition will function as a clearinghouse and share ideas and efforts, although no strong core has materialized as yet. Your TABOR Committee already filed to set up a statewide issue committee (a legal necessity to conform to election requirements). We funded it with seed money and secured a matching donation.

Are you torqued off yet?

Please join the fight by volunteering. Let your interest be known by emailing info@TheTaborCommittee.com or calling 303-747-7460. Please also donate to our efforts by sending a check to the TABOR Coalition at 720 Kipling, Suite 12, Lakewood 80215.

Proposition HH has more pieces to it – a hike in the State revenue and spending limitation that allows government to grow faster than the private sector and a provision about the senior exemption. One of our allies filed a lawsuit because the measure violates the single-subject rule. It has been joined by a dozen local governments!

A different measure on the fall ballot asks voters to allow the State to keep higher marijuana taxes. A provision in TABOR requires proposed tax increases to estimate the amount to be raised. In order to keep governments from monkeying with the estimate, any overage must be returned and the rate adjusted downward, unless the taxpayers in a second vote allow the higher receipts.

There was another anti-TABOR bill that adjusts some definitions on insurance premiums taxes. TABOR does not allow arguments that any higher taxes are too little to care about (de minimis). But, in a lawsuit several years ago filed by the TABOR Foundation (our sister organization), the Colorado Supreme Court errantly imposed a de minimis provision. We cannot fight the precedent set then, and the amount this year truly is small – less than $7,000.

Legislative Democrats have been scheming to kill Colorado’s Taxpayer’s Bill of Rights, or TABOR, since before it was added to the state Constitution in 1992. Hardly a year goes by without a bill, proposal, “listening tour,” or lawsuit hatched to enable state legislators to spend money TABOR denies them. Now, they’re at it again.

Legislative Democrats have been scheming to kill Colorado’s Taxpayer’s Bill of Rights, or TABOR, since before it was added to the state Constitution in 1992. Hardly a year goes by without a bill, proposal, “listening tour,” or lawsuit hatched to enable state legislators to spend money TABOR denies them. Now, they’re at it again.