House Republicans launched a brief filibuster on Friday morning over legislation to double a tax credit using Taxpayer’s Bill of Rights surplus dollars.

House Bill 24-1084 is actually a repeal and re-enactment of a measure from the special session in November that dealt with property taxes. The 2023 measure doubles the Earned Income Tax Credit.

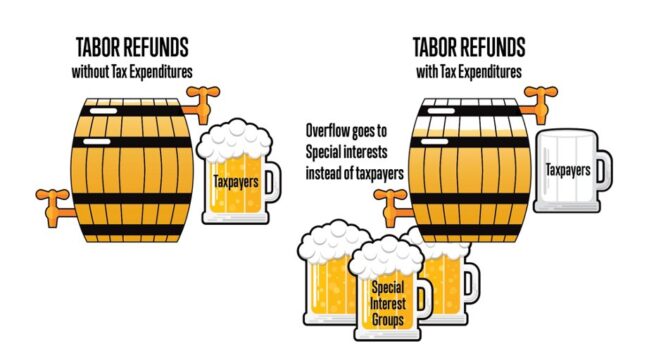

The filibuster, which occurred on just the third day of the new legislative session, lasted about 45 minutes. Republicans’ opposition centers around the bill’s use of TABOR surplus dollars, which they view as an attack on TABOR by reducing refunds by about $182.5 million.

Last year’s bill is the subject of a lawsuit from Rep. Scott Bottoms, R-Colorado Springs. He filed the challenge in Denver District Court on Dec. 28 against House Speaker Julie McCluskie and Gov. Jared Polis, who signed the bill into law, claiming he had been denied his constitutional right to have the measure be read at length during its final vote on Nov. 9.

To continue reading this story, please click (HERE):